HIGHLIGHTS:

- The Fed announced an additional $10 billion per month in tapering, split evenly between Treasuries and MBS.

- The Fed dropped its reference to 6.5% as a threshold for when they would hike short-term interest rates and indicated that they would follow a “broad array” of indicators, including “financial developments”.

- The majority of members of the FOMC still see the first rate hike in 2015, but the pace of rate hikes is projected to be slightly quicker than previously estimated, even though the economic projections were adjusted downward.

- There was one dissenting vote by Kocherlakota who favored sticking with the unemployment and inflation guidelines.

This was the first meeting for Janet Yellen to preside as Chairwoman, but it is also one with some unfilled seats. While there is plenty of uncertainty with many of the voting members in 2014, we think that the overall composition of the FOMC is likely to be more hawkish this year. While we don’t expect a significant change to current policies in the near term, we think that the changes at the Fed could mean we’ll be hearing differing views in the year ahead.

The Fed’s slower pace of bond buying means that its influence on Treasury yields will continue to decline, while the pace of economic growth and inflation prospects are likely to play a larger role in setting policy. We don’t see the shift from the numerical threshold of 6.5% unemployment to more qualitative information is all that different from the Fed’s previous approach. It allows the Fed more flexibility on policy, but may make it more difficult for investors to assess the Fed’s next steps. Treasury bond yields initially moved higher in reaction to the Fed’s statement, perhaps because of the indication that interest rates might move up more quickly once rate hikes begin. However, in her press conference, Yellen explained that the Fed remains committed to reducing unemployment and keeping inflation in check. All in all, our view is that the Fed is still committed to a “measured” approach to changing policy.

Buyout firm Apax Partners LLP stands to score a 10,000 percent gain on its 2005 investment in King Digital Entertainment Plc (KING) as the maker of smartphone game “Candy Crush Saga” prepares its initial public offering.

In one of its last venture capital deals before it abandoned that business, London-based Apax injected about $35 million into King, according to a person with knowledge of the deal, who asked not to be named because the terms are private. The games maker set terms last week for the IPO that would value it at as much as $7.6 billion. Apax’s stake could be worth $3.5 billion.

While Dublin-based King has developed more than 180 games in the past decade, “Candy Crush,” a puzzle game that features colored candies, fueled most of its growth. The potential windfall comes as venture capitalists are seeing their best returns since the late 1990s dot-com bubble. Twelve venture-backed companies went public in the U.S. last year with market capitalizations above $1 billion at the time of offering.

(Source: Bloomberg)

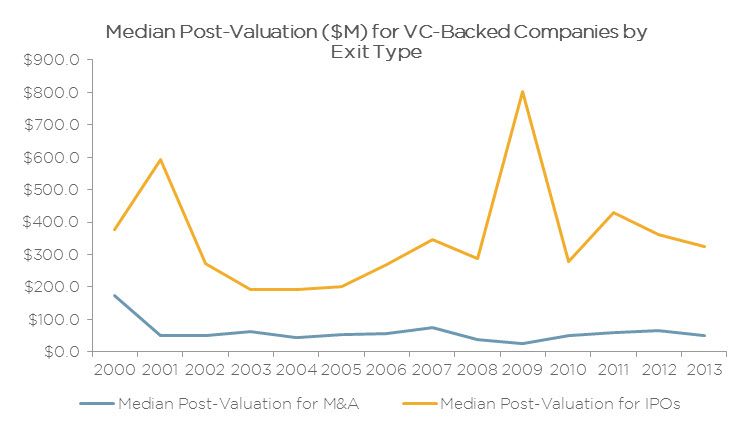

Throughout the early 2000s, the median valuation of companies at IPO was approximately three times larger than it was for companies that were acquired, according to PitchBook data. The difference has been even wider in recent years—greater than 5x each year since 2008 and sitting at 6.5x in 2013.

There are obviously manifold reasons for this development, including that publicly traded stocks have been trading at higher multiples in recent years. Importantly, the increasing discrepancy between the two exit strategies’ valuations cannot simply be attributed to investors pursuing fewer but larger offerings. In fact, the median valuation at IPO has actually declined since 2011 as investors have capitalized on the recent strength in the markets to take more companies public; the 85 IPOs of U.S.-based VC-backed companies in 2013 is the most since the dot-com boom.

Another important consideration when comparing exit valuations is that many mergers & acquisitions will involve struggling companies, and some transactions may not even allow investors to recoup their entire investment. While there are exceptions, companies that go public tend to boast strong performance and strong future growth prospects, which naturally leads to higher valuations.

One notable outlier when it comes to valuations at exit comes in 2009, when the median valuation for VC-backed IPOs came in at a whopping $802 million. This may seem odd, given the low regard investors had for public equities during this period. However, considering that only top-notch companies would risk going public in those conditions, the lofty level of valuations seems more reasonable.

(Source: Pitchbook)

High-yield bond spreads have tightened significantly from the record-wide levels reached during the 2008 financial crisis. However, spreads are still wider than the lows reached in the 2005-2007 period. We believe that high-yield spreads may have some room to tighten further as credit is improving, economy continues to grow, there is a lot of cash on corporate balance sheets and defaults remain low.

(Source: Bloomberg)

Total U.S. crude oil production averaged 7.5 million bbl/d in 2013, 967,000 barrels per day (bbl/d) higher than 2012 and the highest level of U.S. production since 1989. In December 2013, U.S. crude oil production reached 7.9 million barrels per day (bbl/d), according to EIA’s recently released December 2013 Petroleum Supply Monthly, an increase of 785,000 bbl/d (11%) compared with December 2012.

(Source: EIA)

High-frequency trading (HFT) is a type of algorithmic trading, specifically the use of sophisticated technological tools and computer algorithms to rapidly trade securities. HFT uses proprietary trading strategies carried out by computers to move in and out of positions in seconds or fractions of a second. Firms focused on HFT rely on advanced computer systems, the processing speed of their trades and their access to the market.

As of 2009, studies suggested HFT firms accounted for 60-73% of all US equity trading volume, with that number falling to approximately 50% in 2012.

High-frequency traders, move in and out of short-term positions aiming to capture sometimes just a fraction of a cent in profit on every trade. HFT firms do not employ significant leverage, accumulate positions or hold their portfolios overnight; they typically compete against other HFTs, rather than long-term investors. As a result, HFT has a potential Sharpe ratio (a measure of risk and reward) thousands of times higher than traditional buy-and-hold strategies.

HFT may cause new types of serious risks to the financial system. Algorithmic and HFT were both found to have contributed to volatility in the May 6, 2010 Flash Crash, when high-frequency liquidity providers rapidly withdrew from the market. Several European countries have proposed curtailing or banning HFT due to concerns about volatility. Other complaints against HFT include the argument that some HFT firms scrape profits from investors when index funds rebalance their portfolios.

History

Profiting from speed advantages in the market is as old as trading itself. In the 17th century, the Rothschilds were able to arbitrage prices of the same security across country borders by using carrier pigeons to relay information before their competitors. HFT modernizes this concept using the latest communications technology.

High-frequency trading has taken place at least since 1999, after the U.S. Securities and Exchange Commission (SEC) authorized electronic exchanges in 1998. At the turn of the 21st century, HFT trades had an execution time of several seconds, whereas by 2010 this had decreased to milli- and even microseconds. Until recently, high-frequency trading was a little-known topic outside the financial sector, with an article published by the New York Times in July 2009 being one of the first to bring the subject to the public’s attention. On September 2, 2013, Italy became the world’s first country to introduce a tax specifically targeted at HFT, charging a levy of 0.002% on equity transactions lasting less than 0.5 seconds.

In the United States, high-frequency trading firms represent 2% of the approximately 20,000 firms operating today, but account for 73% of all equity orders volume.

As HFT strategies become more widely used, it can be more difficult to deploy them profitably. According to an estimate from Frederi Viens of Purdue University, profits from HFT in the U.S. has been declining from an estimated peak of $5bn in 2009, to about $1.25bn in 2012.

Vincent “Vinnie” Viola, the founder of Virtu Financial Inc, is High Frequency Trading’s (HFT) first billionaire. He has an impressive track record of just “one losing trading day” during a 1,238 trading-day period.

How does he do it? The same way other High-Frequency Traders do it: front running trades and scalping countless billions and billions of fractions-of-pennies in the process.

High-frequency trading could soon officially mint its first billionaire.

Vincent “Vinnie” Viola, the founder of Virtu Financial Inc., could have his stake valued at around $2 billion once the company sells shares to the public, according to two people familiar with the matter.

In a filing Monday, Virtu said it hoped to raise $100 million in an initial public offering, though that figure is just a placeholder that could change based on investor demand. The company will likely seek to raise between $200 million and $250 million, according to the people. At the high end of that range, Virtu would be valued at about $3 billion.

Mr. Viola owns almost 70% of the company. Virtu is hoping that its stellar record – having just “one losing trading day” during a 1,238 trading-day period concluding at the end of December – will grab the interest of investors despite growing scrutiny of the high-frequency trading industry.

Virtu said in its prospectus that the U.S. Commodity Futures Trading Commission was “looking into our trading during the period from July 2011 to November 2013.”

The CFTC is examining Virtu’s “participation in certain incentive programs offered by exchanges or venues during that time period.” Virtu said it didn’t believe it violated any statute or regulatory provision.

The Securities and Exchange Commission has also said it is looking into the impact of high-frequency traders on market stability and fairness.

In addition, a French regulator, Autorité des Marchés Financiers, is examining the 2009 trading activities of a company that eventually became part of Virtu, the prospectus said.

Virtu declined to comment on the regulatory inquiries.

Mr. Viola gained attention last year after paying $240 million for control the Florida Panthers of the National Hockey League. He put his Manhattan mansion on the market for $114 million in December.

(Sources: Various, Wall Street Journal, New York Times)

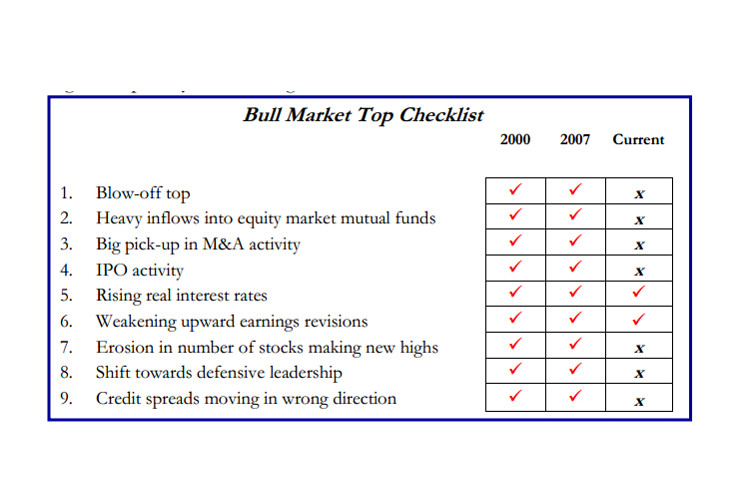

(Source: Strategas)

Investors who are worried about the market’s parabolic rise in the past five years and whether we are at or near a top, can use the above table to judget where we are in the cycle and whether the tide is about to turn the other way.

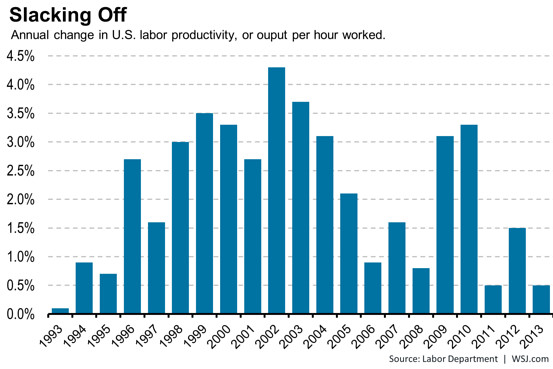

Businesses struggled to squeeze much more out of their workers last year.

A downward revision to fourth-quarter productivity lowered the gain for all of 2013 to just 0.5%, the Labor Department said Thursday. The small increase ties with 2011 for the weakest annual improvement since 1993.

Labor productivity, or output per hour, strengthened early in the economic recovery as businesses grew more efficient. The measure increased 3.1% in 2009 and 3.3% in 2010, to mark the best annual improvement since 2003. But gains have slowed considerably since, measuring 0.5% in 2011 and 1.5% in 2012.

The recent weakness was most pronounced in nondurable manufacturing, a sector that includes the processing of food, chemicals and petroleum, as well as textile and paper production. Sector productivity slipped 0.1% last year because output improvements were more than offset by increased hours worked.

The easing of productivity is a bit of a double-edged sword. The weak gains hold back the economy’s potential to grow. But it also could signal that businesses are finding it more difficult to meet demand with their existing workforce and equipment.

If companies can’t squeeze more out of current workers, they might need to ramp up hiring and capital investment.

(Source: Wall Street Journal)

The downward revision to fourth-quarter GDP growth to 2.3% annualised, compared with the initial 3.2% estimate, was largely due to smaller positive contributions from durables consumption, net exports and inventories, whereas the positive contribution from business investment was actually revised higher. More generally, even a gain of only 2.3% is still impressive in a quarter when the Federal government shutdown resulted in a 5.6% drop in public sector spending, which subtracted more than 1.0% ppts from overall GDP growth.

Durable goods consumption is now estimated to have increased by a more modest 2.5% in the fourth quarter, down from the initial 5.9% estimate. With the bad weather hitting motor vehicle sales hard, we anticipate another modest gain in the first quarter. Net exports are now assumed to have added 1.0% ppt to GDP growth, rather than the initial contribution of 1.3%. Inventories added 0.1%, down from the initial 0.4% estimate.

The good news is that business investment increased by 7.3%, revised up from the initial estimate of a 3.8% gain. that gain helped to offset an 8.7% decline in residential investment, which was hit by the drop back in existing home sales that has reduced brokers’ commissions.