Momentum as an Investment Style

Over the years there has been a significant amount of academic research conducted on the factors driving stock price movements. Researchers have focused on identifying reasons why stocks with certain characteristics tend to outperform persistently. For example, value-oriented stocks (e.g., those having characteristics such as low P/E ratios, high book value-to-market value multiples, etc.) have generated strong consistent outperformance of growth-oriented stocks over time. Eugene Fama and Ken French were among the first to highlight the value factor in 1992 in a seminal paper. Fama and French and others have also highlighted how small caps have outperformed large caps. Besides the value and size factors, several other factors, or styles, have generated statistically significant premiums over long periods of time, including liquidity (e.g., the tendency for less liquid securities to perform better than those that are more liquid), defensive (e.g., stocks that are high quality outperform those of lower quality) and asset growth (e.g., stocks of companies with robust growth in assets underperform those having lower growth).

Momentum has been another style that has performed very well, but hasn’t received the widespread publicity of value and size. The intuition behind momentum as a strategy is that assets that have performed well recently tend to continue to perform well, and conversely, those that have underperformed tend to continue to underperform. In an important 1993 paper, Jegadeesh and Titman first called attention to the momentum factor. In 1997, Carhart added momentum as a factor to the Fama-French three-factor (i.e., market, value and size) model for understanding performance persistence in mutual funds. Like many of the other factors, momentum is evident across many asset classes, including equities, bonds, currencies and commodities.

Momentum portfolios are generally implemented in one of two ways. Some institutional managers will construct long-short portfolios whereby they go long a group of stocks that have been top performers over the recent past, and go short a group of bottom performers. Such a long-short portfolio captures the momentum premium, and has little if any correlation with traditional asset classes. Some managers, such as AQR, have created portfolios extracting momentum across a diverse set of asset classes, which because of the lack of correlation, creates an overall strategy with attractive risk-adjusted returns. The other primary way of implementing a momentum strategy is simply to go long the group of recent top performers, foregoing the short portfolio. While this strategy has significant beta exposure, it is more easily implemented for investors who either cannot, or prefer not to, use short positions.

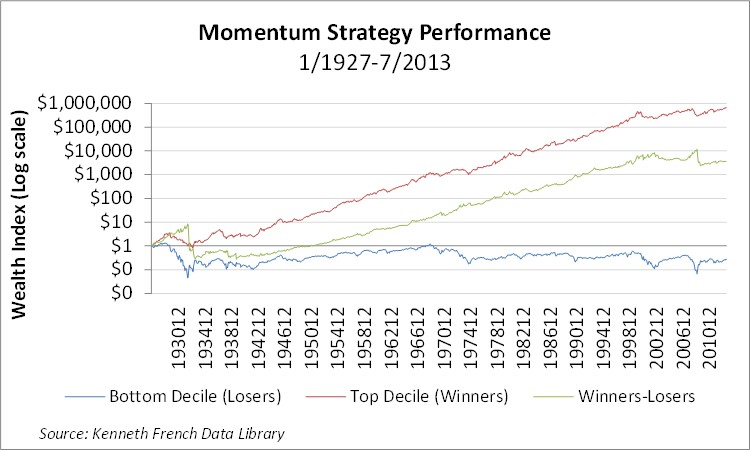

The graph below shows the performance of the top decile stocks (“winners”), the bottom decile stocks (“losers”), and the long-short portfolio of “winners” minus “losers” over the period covering January 1927 through July 2013.