6

Japanese shares closed at a six-year high Tuesday, propelled steadily upward as investors look to developed Asia for returns and show growing faith in Japan’s reform agenda.

(Source: Wall Street Journal)

Japanese shares closed at a six-year high Tuesday, propelled steadily upward as investors look to developed Asia for returns and show growing faith in Japan’s reform agenda.

(Source: Wall Street Journal)

One of the primary decisions investors and their advisors are faced with in the portfolio construction process is the type of investment approach – active or passive – to employ. Is there value to be added in hiring active managers, or should a portfolio be passively constructed in order to simply gain the desired market exposures in a cost-efficient manner? Or perhaps a superior outcome can be achieved through a “core/satellite” approach, in which the components of the allocation representing the more efficient market segments are passively invested while active managers are selected for the satellite exposures where inefficiencies may be more prevalent. If so, which asset classes might best be designated as “passive” and which ones “active”? To add complexity, if a decision is made to employ some element of active management, the investor and advisor must then select specific managers to comprise those allocations.

Over the years, there has been a significant amount of research conducted on the active vs. passive question. The debate has generally boiled down to being a referendum on the merits of the efficient market theory (EMT), which posits that since market prices instantaneously react to the knowledge and expectations of all investors, it is impossible to systematically outperform the benchmark consistently. Adherents of EMT typically favor passive management and employ ETFs, index funds and other passive strategies in the portfolio construction process. On the other side of the debate are those that point to the long-term success of certain active managers such as Warren Buffett, Peter Lynch and John Templeton as evidence that markets are not efficient and that active management can indeed add value.

Conclusions from the results of a recent study on this topic: (1) certain Morningstar categories exhibit incidence of manager skill over time, and are therefore candidates for active management; (2) the alphas of the skilled group of managers are not only statistically, but also economically significant; (3) the incidence of manager skill is different for foreign and domestic equities across various economic environments; and (4) in terms of manager selection within categories designated as active, the best dimensions that predict future manager performance are the previous period’s active return, expense ratio and capture ratio.

Overall, our results tend to support the core/satellite approach to portfolio construction. The core (more efficient) categories such as those within the domestic large cap equity segment warrant passive allocation, while the satellite (less efficient) categories such as domestic small cap and international developed and emerging markets are good candidates for active management.

A third of Americans will return at least one gift after the holidays, according to a FedEx survey.

(Source: Wall Street Journal)

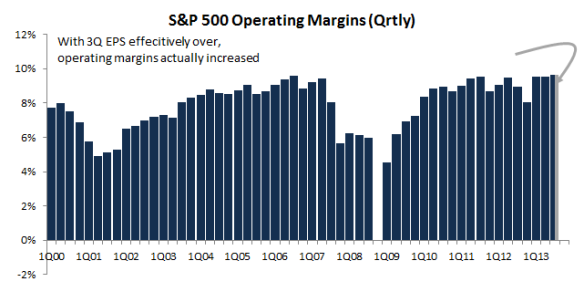

Do you think that the high Operating Margins will hold in 2014?

The major drivers for the high Operating Margins in 2013, viz. productivity, technology and cheap imports, should help again next year. Other factors like cheap energy and lower effective tax rates should continue to help as well. Plus, we do not see excesses in business investment, inventory or debt (personal or commercial) in 2014.

Persistently high profit margins should help equities in 2014.

Mark Zuckerberg will likely pocket about $1 billion from his first stock sale since Facebook’s initial public offering, part of a complex transaction in which the founder and chief executive also plans to donate stock valued at roughly $1 billion to charity.

(Source: Wall Street Journal)

The conviction of SAC’s Michael Steinberg marks the latest victory for U.S. prosecutors in their campaign against insider trading, which has resulted in 77 guilty pleas or convictions over the past four years.

(Source: Wall Street Journal)

On December 18, 2013, the Federal Open Market Committee (FOMC) directed the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York to purchase additional agency mortgage-backed securities (MBS) at a pace of about $35 billion per month and longer-term Treasury securities at a pace of about $40 billion per month, beginning in January 2014. The existing December schedules for agency MBS purchases at a pace of $40 billion per month and Treasury securities purchases at a pace of $45 billion per month remain in effect until that time. The FOMC also directed the Desk to maintain its existing policies of reinvesting principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in agency MBS and of rolling over maturing Treasury securities at auction. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

Purchases of agency MBS will continue to be concentrated in newly-issued agency MBS in the To-Be-Announced (TBA) market, and purchases of longer-term Treasury securities will continue to be distributed using the existing set of sectors and approximate weights. These purchase distributions could change if market conditions warrant.

The amount of agency MBS to be purchased each month and the tentative schedule of Treasury purchase operations for the following calendar month will continue to be announced on or around the last business day of each month. Additionally, the planned amount of purchases associated with reinvestments of principal payments on holdings of agency securities that are anticipated to take place over each monthly period will be announced on or around the eighth business day of the month.

Consistent with current practices, the purchases of agency MBS and Treasury securities will be conducted with the Federal Reserve’s eligible counterparties through a competitive bidding process and results will be published on the Federal Reserve Bank of New York’s website. The Desk will continue to publish transaction prices for individual operations at the end of each monthly period. All other purchase details remain the same at this time.

Additional information on the purchases of agency MBS and longer-term Treasury securities can be found in a set of Frequently Asked Questions for each asset class in the following locations:

The BalticDry Index is issued daily by the London-based Baltic Exchange and provides “an assessment of the price of moving the major raw materials by sea”, like, iron ore, coal, grain, cement, copper, sand and gravel, fertilizer and even plastic granules.

Since it targets real-time shipping rates, which fluctuate based on supply and demand, subjectivity can’t creep into the readings. Day in and day out, it provides a snapshot of global economic activity at the earliest possible stage.

Year-to-date, the index is up nearly 230%. It now rests at its highest level since late 2010.

Can this be a sign of global recovery improving in 2014?

11%

The American Bar Association said on Tuesday that the number of first-year law students fell 11% this year across the 202 U.S. law schools that the group accredits—plunging to levels not seen since the 1970s.

(Source: Wall Street Journal)

2,200

The Energy Department in the U.S. blocked about 2,200 attempts this year by users seeking to get data from its websites in ways that endangered equal access to the agency’s widely followed economic reports.