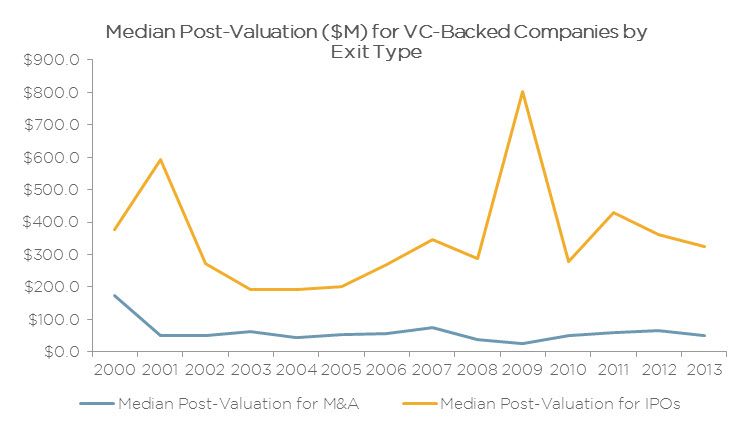

Throughout the early 2000s, the median valuation of companies at IPO was approximately three times larger than it was for companies that were acquired, according to PitchBook data. The difference has been even wider in recent years—greater than 5x each year since 2008 and sitting at 6.5x in 2013.

There are obviously manifold reasons for this development, including that publicly traded stocks have been trading at higher multiples in recent years. Importantly, the increasing discrepancy between the two exit strategies’ valuations cannot simply be attributed to investors pursuing fewer but larger offerings. In fact, the median valuation at IPO has actually declined since 2011 as investors have capitalized on the recent strength in the markets to take more companies public; the 85 IPOs of U.S.-based VC-backed companies in 2013 is the most since the dot-com boom.

Another important consideration when comparing exit valuations is that many mergers & acquisitions will involve struggling companies, and some transactions may not even allow investors to recoup their entire investment. While there are exceptions, companies that go public tend to boast strong performance and strong future growth prospects, which naturally leads to higher valuations.

One notable outlier when it comes to valuations at exit comes in 2009, when the median valuation for VC-backed IPOs came in at a whopping $802 million. This may seem odd, given the low regard investors had for public equities during this period. However, considering that only top-notch companies would risk going public in those conditions, the lofty level of valuations seems more reasonable.

(Source: Pitchbook)