2,200

The Energy Department in the U.S. blocked about 2,200 attempts this year by users seeking to get data from its websites in ways that endangered equal access to the agency’s widely followed economic reports.

12

Twelve movies are set to open at 500 theaters or more between Dec. 12 and 25, the highest number in recent times.

(Source: Wall Street Journal)

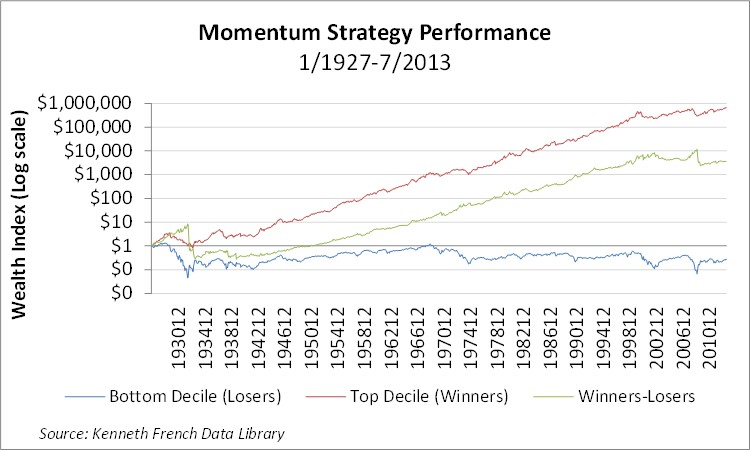

Momentum as an Investment Style

Over the years there has been a significant amount of academic research conducted on the factors driving stock price movements. Researchers have focused on identifying reasons why stocks with certain characteristics tend to outperform persistently. For example, value-oriented stocks (e.g., those having characteristics such as low P/E ratios, high book value-to-market value multiples, etc.) have generated strong consistent outperformance of growth-oriented stocks over time. Eugene Fama and Ken French were among the first to highlight the value factor in 1992 in a seminal paper. Fama and French and others have also highlighted how small caps have outperformed large caps. Besides the value and size factors, several other factors, or styles, have generated statistically significant premiums over long periods of time, including liquidity (e.g., the tendency for less liquid securities to perform better than those that are more liquid), defensive (e.g., stocks that are high quality outperform those of lower quality) and asset growth (e.g., stocks of companies with robust growth in assets underperform those having lower growth).

Momentum has been another style that has performed very well, but hasn’t received the widespread publicity of value and size. The intuition behind momentum as a strategy is that assets that have performed well recently tend to continue to perform well, and conversely, those that have underperformed tend to continue to underperform. In an important 1993 paper, Jegadeesh and Titman first called attention to the momentum factor. In 1997, Carhart added momentum as a factor to the Fama-French three-factor (i.e., market, value and size) model for understanding performance persistence in mutual funds. Like many of the other factors, momentum is evident across many asset classes, including equities, bonds, currencies and commodities.

Momentum portfolios are generally implemented in one of two ways. Some institutional managers will construct long-short portfolios whereby they go long a group of stocks that have been top performers over the recent past, and go short a group of bottom performers. Such a long-short portfolio captures the momentum premium, and has little if any correlation with traditional asset classes. Some managers, such as AQR, have created portfolios extracting momentum across a diverse set of asset classes, which because of the lack of correlation, creates an overall strategy with attractive risk-adjusted returns. The other primary way of implementing a momentum strategy is simply to go long the group of recent top performers, foregoing the short portfolio. While this strategy has significant beta exposure, it is more easily implemented for investors who either cannot, or prefer not to, use short positions.

The graph below shows the performance of the top decile stocks (“winners”), the bottom decile stocks (“losers”), and the long-short portfolio of “winners” minus “losers” over the period covering January 1927 through July 2013.

54%

That is U.S. President Barack Obama’s disapproval rating—an all-time high, even as Americans feel more upbeat about the economy.

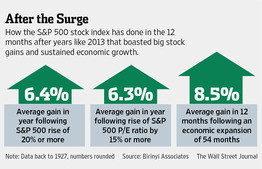

History seems to support the idea that 2014 will be less historic than 2013. Since 1927, there have been 23 years in which the S&P 500 has risen 20% or more, according to Birinyi Associates. It averaged a further gain of 6.4% in the next year. That is only slightly better than the 5.5% gain the S&P averaged for all years since 1927.

On only one of those 23 occasions of 20%-plus annual gains did the S&P improve its performance in the following year. In 1997 it rose 31% after a 20% gain in 1996. It rose again in 1998, by 27%, and in 1999, by 20%. Those were the days.

The S&P 500 has been known to decline in the year after a 20% gain. That has happened eight times. Six times it put in another 20% gain.

Data comparing the expansion of the S&P 500’s price/earnings ratio with past years, and comparing the performance at the current stage in the economic cycle, suggest gains of 6% to 9%.

It is possible that 2014 will be another year like 1997 and stocks will rise even faster than in 2013. Many in the market think the new Fed chairwoman, Janet Yellen, slated to take office Feb. 1 pending Senate confirmation, will delay withdrawing stimulus and fuel another big market year.

But before betting that 2014 will be better than 2013, investors might consider that it has happened once since 1927.

(Source: Wall Street Journal)

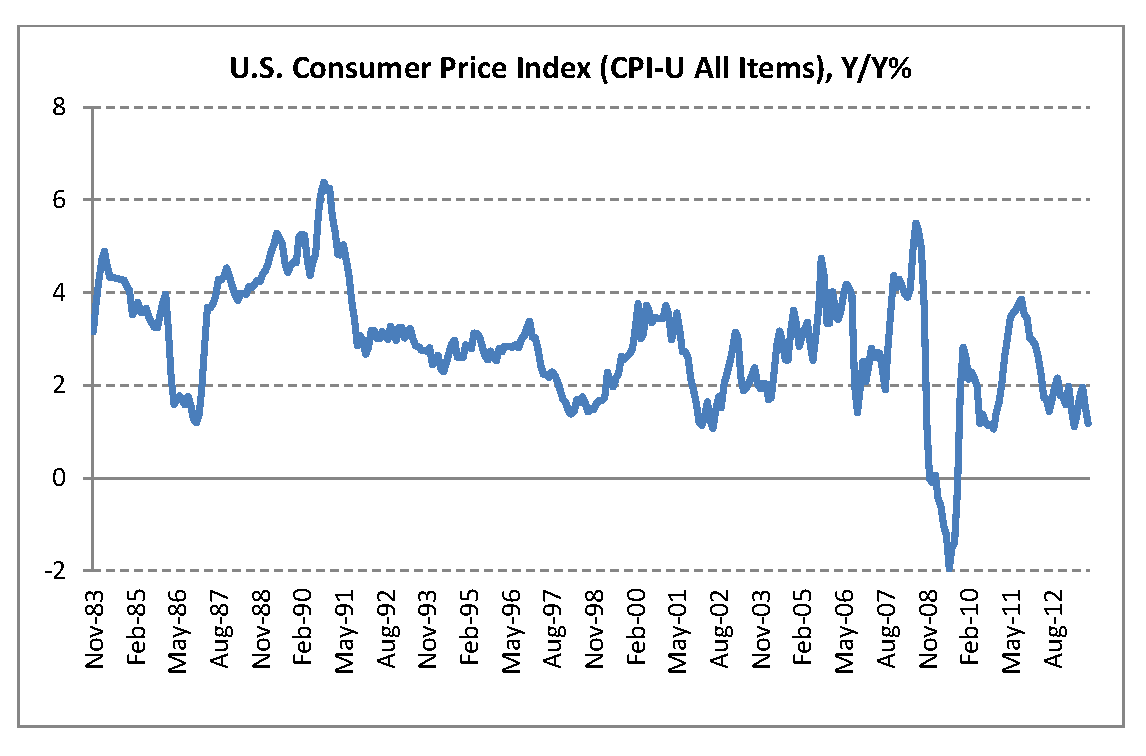

Inflation in the U.S. has been tame. According to the Consumer Price Index (CPI), prices have increased only +1.2% over the last 12 months, below the Fed’s target of 2% inflation. Tame inflation will allow the Fed to remain accommodative for longer.

91

That is how many heads of state are expected to attend Nelson Mandela’s memorial service in Johannesburg Tuesday.

(Source: Wall Street Journal)

When the US Dollar has rallied in the past, real assets, especially gold and commodities have performed poorly, as the following table shows. Although real assets can provide a hedge against a weak dollar, they also can underperform when the dollar strengthens. Similarly, although real assets can provide some protection against inflation, they can also perform poorly when inflation is low. And in the current low-growth environment, inflation has been declining, according to data from the Bureau of Economic Analysis, and some observers believe it could remain low for a while despite the Fed’s easy money policy.

Source: Morningstar. Data as of November 2013.

1 U.S. Dollar Index (DXY).

2 S&P GSCI Gold Total Return Index.

3 S&P GSCI Total Return Index.

4 Barclays U.S. Corporate Baa Bond Total Return Index.

5 S&P 500 Total Return Index.

Past performance is no guarantee of future results.

The historical data are for illustrative purposes only, do not represent the performance of any particular investment, and are not intended to predict or depict future results. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment. Performance during other time periods may be different or negative. Investors may experience different results. Due to market volatility, the market may not perform in a similar manner in the future.

6.8%

How much in dollar terms that store sales of zero- and low-calorie soda plunged in the 52 weeks through Nov. 23, while sales of regular sodas dropped 2.2%. Diet soda demand has contracted more than regular soda for three straight years.

(Source: Wall Street Journal)